So, you’re wanting to purchase your first home and are concerned you may not have enough savings? It’s a common worry for many first home buyers. Let’s face it, it’s hard saving for a deposit, particularly if you’re paying rent or paying off a HECS or HELP debt.

In this FHB Q&A, we provide inside expert knowledge on what the banks are looking for from first home buyers, as well as other government grants available such as the First Home Loan Deposit Scheme (FHLDS), enabling FHB’s the ability to buy their first home with only 5% deposit.

First, it’s important to acknowledge that there are many lenders that want to help first home buyers get into their first home. In fact, we have over 40 lenders on our panel that can provide some great home loan options for first home buyers with many accredited to offer a place on the FHLDS.

Let’s take a look at how your savings will affect your ability to secure a home loan;

Genuine savings

The first question most banks will ask is “does the applicant have genuine savings?”. So, what are genuine savings as opposed to non-genuine savings? The ‘genuine’ component refers to the length of time those savings have accumulated.

If you have been putting money aside into a separate savings account on a regular basis, let’s say, $400 per week for the last 12 months to save for a deposit, there is a clear and visible history of those savings accumulating. This tells the bank that you can manage your money well and have the discipline to save.

Non-genuine savings would include things like money received from the sale of an asset, bonuses, an inheritance or a tax refund – essentially a lump sum for a transaction. These types of savings are one off payments and don’t show a money managing habit.

The good news is, you can combine both genuine and non-genuine savings to form your deposit. However, you must show at least three months of genuine savings. So, start squirrelling that money away and if possible, move that money to a dedicated savings account so the bank can see clearly that you’re good at money management.

Rent vs Savings

Each lender looks at a customer differently, some will consider your weekly rent or board payments as a form of savings. Yes, you heard us, some banks consider the rent you’ve been paying for years as a type of savings!

“Dead money you’ve been paying your landlord can, on paper, be taken into account as part of your savings history.”

For those who are buying their first home to live in, the requirement to pay a landlord rent is removed once you move in, so the ability to show a rental history shows the bank that you had the money management skills to keep up your rental repayments, and therefore would have had the ability to save that money if you weren’t renting.

Minimum deposit needed to buy your first home

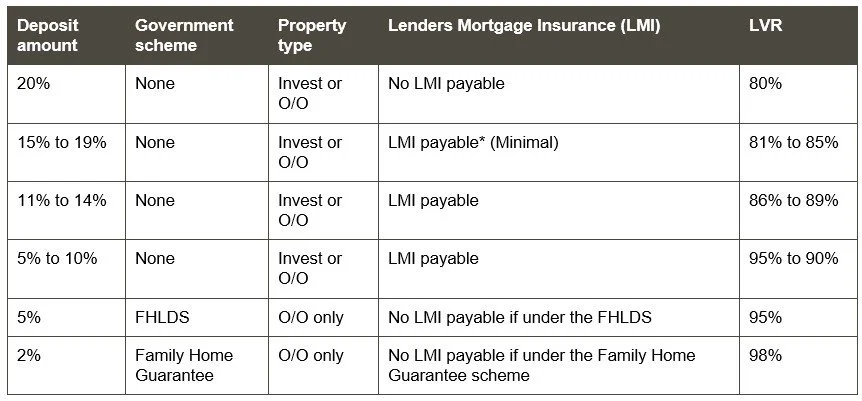

There is a common misconception that you need 10% deposit to buy a home. That is simply not true. However, there are additional costs including Lenders Mortgage Insurance (LMI) if you don’t have the full 15-20% deposit.

LMI is a fee the borrower pays if they don’t have 20% deposit. The ‘insurance’ is actually to protect the bank, not the borrower, even though it’s the borrower who pays the insurance premium.

There are some lenders that offer a very low LMI fee for borrowers with a 15% deposit.

And for those First Home Buyers who only have 5% deposit, the FHLDS means the Australian Government will cover the LMI costs for those on the scheme.

Single parents also have the opportunity to buy a property with only 2% deposit under the Family Home Guarantee. This scheme allows eligible single parents with at least one dependent child in purchasing the family home. The Family Home Guarantee isn’t restricted to first home buyers, as the scheme allows for borrowers who have previously owned a property but don’t currently own one.

Below is a table showing how your deposit amount affects your requirement to pay LMI.

Invest = Investment (ie, you can rent out the property)

O/O = Owner Occupied (ie, you live in it)

LVR = Loan to Value Ratio

* LMI payable (Minimal) = some lenders have promotions offering $1 LMI fees. LMI is calculated on a sliding scale.

Guarantor loans or the ‘bank of mum and dad’

You may have heard of a ‘family guarantee’ or in the media, they refer to it as ‘the bank of mum and dad’. Essentially a family member, can use the available equity in their parents’ home as a deposit.

A family guarantee can be used to fund part of the deposit or all of it. This is a popular option for family members wanting to help their kids get a kick start into the property market.

So, how does a guarantor loan work?

Let’s say mum and dad have a property valued at $1,500,000 and they have a $200,000 mortgage on the property, the equity would be $1,300,000. However, only 80% of the equity can be used, so that would mean there is $1,040,000 of available equity to go towards the deposit for another property purchase.

So, let’s say the first home buyer has 5% deposit for an $800,000 property purchase ($40,000), and they would like to avoid paying LMI (see above table), mum and dad can guarantee the remaining 15% deposit funds ($120,000). Combining the $40,000 and $120,000 deposits against the purchase would reduce the LVR to 80% - removing the need to pay LMI.

By reducing the LVR to 80%, the borrower saves $35,000 on LMI.

Working with a proactive mortgage broker like Mint Equity will enable the guarantors and borrowers property values to be regularly reviewed, to see if there is enough equity in the newly acquired property to release the guarantor from the loan.

Final tip

When it comes to credit policies including genuine and non-genuine savings and rent/board payments being considered savings, no lender is the same and most of these policies are subject to the interpretation of the credit assessor. This is why it’s so important to work with an experienced mortgage broker like Mint Equity who can guide you through the ins and outs of the lending world.

Contact us to set up a time to chat and get guidance to set you on the right path to saving for your first home.